Renting your first apartment is a significant milestone, marking a transition to independence and self-reliance. However, navigating the financial landscape of renting can be daunting, especially for first-time renters. This comprehensive guide, “How to Budget for Renting Your First Apartment,” will provide you with the essential tools and knowledge to successfully plan and manage your finances, ensuring a smooth and stress-free renting experience. We’ll cover crucial aspects, including calculating affordable rent, understanding rental costs like security deposits and utilities, and creating a realistic budget that incorporates all your living expenses. Learn how to budget for an apartment effectively and embark on your renting journey with confidence.

From estimating moving costs to creating a savings plan, this guide will address all the key financial considerations involved in renting your first apartment. We will delve into the importance of renter’s insurance, discuss negotiating lease terms, and provide practical advice on managing unexpected expenses. Whether you’re unsure how to calculate your debt-to-income ratio or need guidance on building your credit score, this guide will equip you with the necessary information to make informed decisions and secure your first apartment. Start planning your apartment budget today and take the first step towards a successful and financially secure renting experience.

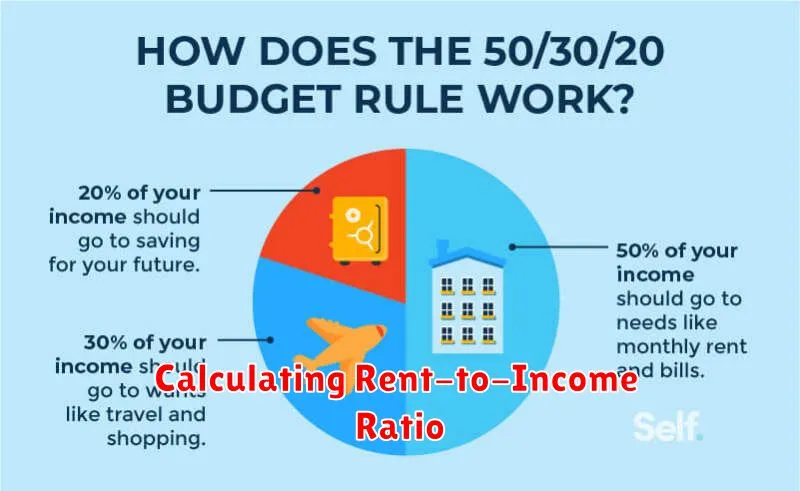

Calculating Rent-to-Income Ratio

Your rent-to-income ratio is a crucial factor in determining how much rent you can comfortably afford. It’s the percentage of your gross income (before taxes and deductions) that goes towards rent.

The most common recommendation is the 30% rule, suggesting that your rent should not exceed 30% of your gross monthly income. For example, if you earn $4,000 per month before taxes, your rent ideally shouldn’t exceed $1,200 ($4,000 x 0.30 = $1,200).

Some landlords may use the 50/30/20 rule, a broader budgeting guideline where 50% of your income goes to needs (including rent), 30% to wants, and 20% to savings and debt repayment. Using this guideline allows for variations based on individual financial priorities.

To calculate your rent-to-income ratio, divide your monthly rent by your gross monthly income, then multiply by 100 to express it as a percentage. For instance, if your rent is $1,000 and your gross income is $3,500, your rent-to-income ratio is approximately 28.6% ([$1,000 / $3,500] x 100 = 28.6%).

Estimating Utilities and Internet Costs

In addition to rent, you’ll need to budget for utilities and internet. These can vary significantly based on your location, apartment size, and usage habits. It’s crucial to factor these costs into your overall budget to avoid financial surprises.

Common Utilities include:

- Electricity

- Gas (for heating and/or cooking)

- Water

- Trash/Sewage

Some apartments include some or all utilities in the rent, so clarify this with your landlord. If not, you can estimate these costs by contacting local utility providers or asking similar apartments in the area.

Internet service is essential these days. Research providers and plans available in your area. Costs vary based on speed and data limits. Consider your needs and budget accordingly.

Factoring in Deposits and Move-In Fees

Beyond monthly rent, anticipate upfront costs like security deposits and move-in fees. A security deposit typically covers potential damages to the unit and can equal one or two months’ rent. Landlords are required to return this deposit, minus deductions for necessary repairs, after you move out. Be sure to document the condition of the apartment with photos and/or video when you move in and out.

Move-in fees, sometimes called administrative fees, cover the landlord’s costs for processing your application and preparing the unit. These fees can vary significantly, so inquire about them upfront.

Budgeting for these costs is crucial. Consider setting aside a separate savings fund specifically for these one-time expenses. Factor these into your overall moving budget to avoid financial surprises.

Allocating for Groceries and Essentials

Groceries and essential household items constitute a significant portion of your monthly expenses. Accurately estimating these costs is crucial for a successful budget. Track your current spending for a few weeks to get a baseline, or use online grocery platforms to estimate costs based on your typical shopping list.

Factor in variables like dietary restrictions, preferred brands, and household size. A single person’s grocery bill will differ significantly from a family’s. Don’t forget essential non-food items like cleaning supplies, personal hygiene products, and toiletries.

Consider creating a separate budget category specifically for these essentials. This allows for clearer tracking and adjustments as needed. Be prepared to adjust your grocery budget periodically to account for fluctuations in food prices.

Budgeting for Furniture and Setup

Furnishing your first apartment can be a significant expense. It’s essential to budget appropriately to avoid overspending. Start by creating a list of essential furniture items.

Consider purchasing used furniture to save money. Check online marketplaces, thrift stores, and consignment shops for affordable options. Don’t feel pressured to furnish everything at once. Prioritize essential items like a bed, sofa, and table and chairs. You can add other pieces gradually as your budget allows.

Set a realistic budget for each item. Research prices online and in stores to get an idea of how much things cost. Be prepared to compromise. You may not be able to afford everything you want right away.

Setting Aside Emergency Savings

Emergency savings are crucial, especially when renting your first apartment. Unexpected expenses, such as job loss or medical bills, can quickly derail your finances. Having a safety net will provide a buffer against these unforeseen circumstances and prevent you from falling behind on rent or other essential bills.

Aim for at least three to six months’ worth of living expenses in your emergency fund. This amount will cover essential costs like rent, utilities, groceries, and transportation if your income is interrupted.

Start small if building a substantial emergency fund seems daunting. Even setting aside a small amount each month will add up over time. Consider automating your savings by setting up regular transfers from your checking account to a dedicated savings account.

Using Budgeting Apps to Stay on Track

Budgeting apps can be invaluable tools for managing your finances, especially when renting your first apartment. They provide a centralized platform to track income and expenses, making it easier to visualize where your money is going.

Many apps offer features like automated bill reminders, which help avoid late fees. Some can even categorize your spending automatically, revealing potential areas for savings. This is particularly useful for identifying non-essential expenses that might be impacting your ability to save for rent and other important costs.

Choosing the right app is key. Consider factors like ease of use, available features, and whether it integrates with your bank accounts. Some popular options include Mint, YNAB (You Need a Budget), and Personal Capital.

{kind=link}